Your Stress-Free Guide to Shopping for Home Loans

In Buy a Home: Step-by-StepWith this super-simple breakdown of loan types, you’ll find the right mortgage.

Costly mistakes happen during this step. Be super-picky about who your lender is.

With this super-simple breakdown of loan types, you’ll find the right mortgage.

Someone out there wants to help save you time, stress, and money. Here’s how you find them.

Your questions answered: four Q&As on Facebook with real estate experts.

One of the biggest misconceptions of home buying? The 20% down payment. Here’s how to buy with a lot less down.

Tight-fisted lenders have made home equity loans harder to come by. So what’s a fixer-upper to do? Meet the 203(k) loan.

Private mortgage insurance is unavoidable for some homeowners, but don’t pay PMI premiums a day longer than required by your lender.

To manage your biggest asset, create a financial plan that covers repairs, upgrades, mortgages, insurance, and taxes.

You can refinance or recast your mortgage. Or you can create your own DIY mortgage restructuring plan. We compare so you can decide.

Taking out a home equity loan against the value of your property can backfire if you fail to avoid these common pitfalls in the borrowing process.

Interest rates are only one factor when it comes to buying a house now.

You’ve got options, like repayment help from your employer and coaching from a mortgage broker.

Home buyers who do mortgage loan shopping can avoid leaving money on the table.

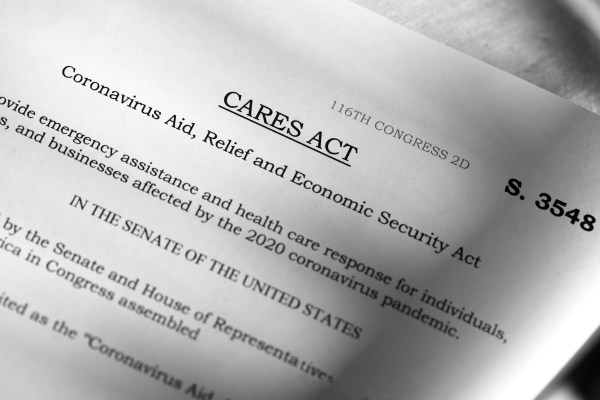

It’s a confusing time, but lenders are putting remedies, like forbearance, in place to help homeowners.

Whether you’re self-employed or applying for an FHA or USDA loan, here’s the pre-approval paperwork you need.

The credit score to buy a house can be as low as 580.

And used a VA loan, which has more restrictions than a conventional one.